Financing Tech in Germany and France in 2025

Financing Tech in Germany and France in 2025

The AI funding race is entering its industrial phase

Berlin, Paris – 22nd of February 2026 – IRIS, a leading European Venture and Growth investment firm, publishes the 2025 edition of “Financing Tech in Germany and France”.

By comparing Europe’s two largest tech and industrial economies over four consecutive years, relying on Dealroom data, the study shows that beyond cyclical fluctuations in funding volumes, European competitiveness is now defined by what capital is deployed for, not just where it is invested.

In 2025, France and Germany are undergoing the same structural transition: from software-led innovation to the transformation of real economic systems, while following two distinct execution paths.

Behind similar macro dynamics -capital concentration, rising AI intensity and tougher scaling conditions, the two countries reveal different ways of turning technology into economic performance and European competitiveness.

Fewer rounds, bigger bets: building Europe’s next tech champions

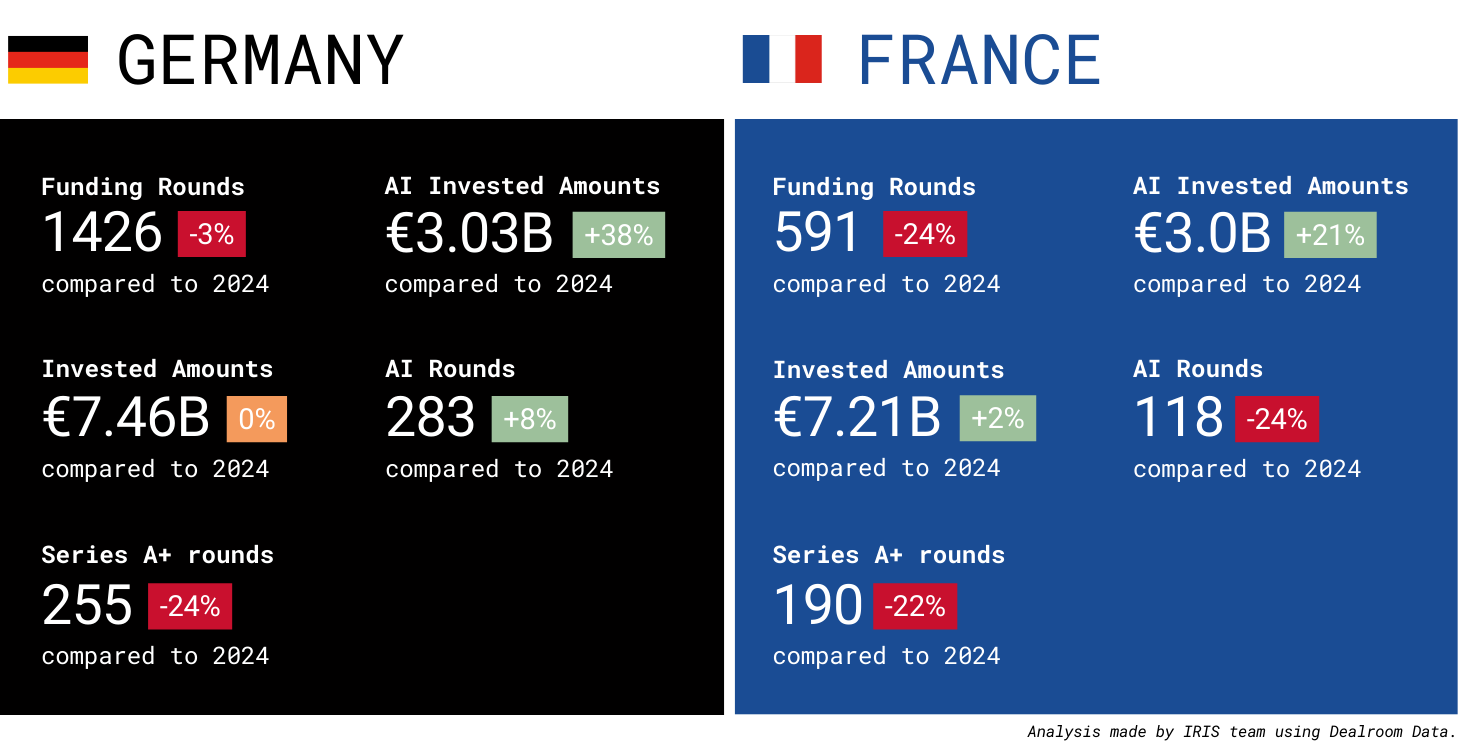

In 2025, total tech investments reached €7.21 billion in France (+2%) and €7.46 billion in Germany (stable year-on-year), despite a sharp contraction in deal activity (591 rounds in France, -24%; 1,426 rounds in Germany, -3%). This apparent paradox reflects a new competitive funding regime: fewer deals, but larger and more execution-intensive rounds.

Capital concentration has reached historically high levels. The Top 10 rounds accounted for 37% of total capital deployed in France (€2.58B) and 31% in Germany (€2.34B). The structure of this concentration differs markedly across the two markets. In Germany, all Top 10 rounds exceeded €100M (with 10th Solaris at €140M), while in France only six of the Top 10 rounds were above €100M, with the 10th at €70M (Intact). This gap illustrates two approaches to scale: broad-based large rounds in Germany versus a more polarised concentration in France.

AI sits at the core of this shift. In 2025, AI investments reached €3 billion in France (+21%) and €3.03 billion in Germany (+38.3%), even as AI deal volumes declined in France (118 rounds, -24.4%) and increased modestly in Germany (283 rounds, +7.8%). This divergence confirms a decisive evolution: AI investment is no longer exploratory, but capital-intensive, infrastructure-driven and focused on real-economy deployment.

Focus on France: competitiveness through concentration and execution depth

France illustrates the most concentrated version of this transition. Out of €7.21 billion invested in French startups in 2025, €2.4 billion went to enterprise software tagged companies, and €1.7 billion to Mistral AI, nearly four times its 2024 funding (€468M). This level of concentration signals a clear shift: competitiveness is now built around a very limited number of execution-heavy platforms rather than broad application-layer innovation.

This dynamic is reinforced by the rapid rise of capital-intensive sectors. Semiconductors recorded one of the strongest accelerations (+420%), driven by next-generation hardware and computing rounds such as Alice & Bob (€100M) and Scintil Photonics (€50M), alongside a growing cluster of mid-sized industrial deeptech rounds. Robotics surged by +325%, supported by financings including Genesis AI (€95M) and Wandercraft (€68M), directly linking AI to industrial and healthcare execution.

Beyond enterprise software, health (€1.1B) and fintech (€715M) continued to attract substantial capital, particularly for payments infrastructure, compliance, diagnostics and biotech. The sustained presence of energy, transportation and food among the top funded sectors further confirms that, in France, AI is increasingly deployed as an optimisation and control layer within long-cycle physical systems, rather than as a standalone product.

Focus on Germany: competitiveness through diffusion and industrial scale

In Germany, €7.46 billion were invested in tech companies in 2025, following a more distributed model of capital deployment. Investment is spread across sectors, closely aligned with the country’s industrial backbone, supporting scale through interoperability and system-wide upgrading rather than platform concentration.

Robotics and education stand out as the strongest accelerators. Robotics funding jumped +432%, with deal count rising from 7 to 23, led by large rounds such as Quantum Systems (€340M), NEURA Robotics (€120M) and STARK (€56M), reinforcing Germany’s competitive edge in automation, defence and industrial equipment. Education technologies also rebounded strongly, reflecting renewed investor focus on workforce transformation, vocational training and enterprise learning - now viewed as essential competitiveness infrastructure in a technology-intensive economy.

Germany’s model is characterised by industrial diffusion: tech capital is embedded across manufacturing, logistics, energy systems and organisational processes, enabling long-term productivity gains across the real economy.

AI moves down the stack: one transition, two execution models

Across both countries, AI now represents a significant share of capital deployed in enterprise software, fintech, health, security and transportation, confirming its role as a core driver of performance rather than a technological option. In more infrastructure-heavy sectors such as energy, food and parts of transportation, AI adoption appears less visible in funding data, not due to weaker uptake, but because AI operates primarily as an operational layer, enhancing efficiency, predictability and resilience over long execution cycles.

“Once more, comparing tech investments in France and Germany proves that European competitiveness in AI is not built on a single model. France illustrates a more concentrated approach, where capital is deployed to accelerate execution in a limited number of large, execution-heavy projects. Germany, by contrast, follows a broader diffusion model, embedding innovation across its industrial backbone. Different paths, but the same requirement: the ability to quickly deploy AI at scale within real economic systems, over time and with direct results to justify the massive corporate investments.” explains Julien-David Nitlech, Managing Partner, IRIS

“It is now time to act. We must now significantly boost the funding capacity of French and German startups - an essential condition for innovative projects to scale and enhance Europe’s competitiveness in the international innovation race. Late-stage financing is indeed crucial for supporting startups in their scale-up phase. However, Series A+ fundraising has declined by 22% in France and 24% in Germany. We need to reverse this trend. And that’s what happens during the next VivaTech’s edition with Germany being “Country of the Year”. Thanks to a common Franco-German innovation ecosystem presentation, we are creating the necessary conditions for supporting the emergence of future European champions” declares Patrick Brandmaier, Managing director of the French-German Chamber of Commerce and Industry

Berlin, Paris – 22nd of February 2026 – IRIS, a leading European Venture and Growth investment firm, publishes the 2025 edition of “Financing Tech in Germany and France”.

By comparing Europe’s two largest tech and industrial economies over four consecutive years, relying on Dealroom data, the study shows that beyond cyclical fluctuations in funding volumes, European competitiveness is now defined by what capital is deployed for, not just where it is invested.

In 2025, France and Germany are undergoing the same structural transition: from software-led innovation to the transformation of real economic systems, while following two distinct execution paths.

Behind similar macro dynamics -capital concentration, rising AI intensity and tougher scaling conditions, the two countries reveal different ways of turning technology into economic performance and European competitiveness.

Fewer rounds, bigger bets: building Europe’s next tech champions

In 2025, total tech investments reached €7.21 billion in France (+2%) and €7.46 billion in Germany (stable year-on-year), despite a sharp contraction in deal activity (591 rounds in France, -24%; 1,426 rounds in Germany, -3%). This apparent paradox reflects a new competitive funding regime: fewer deals, but larger and more execution-intensive rounds.

Capital concentration has reached historically high levels. The Top 10 rounds accounted for 37% of total capital deployed in France (€2.58B) and 31% in Germany (€2.34B). The structure of this concentration differs markedly across the two markets. In Germany, all Top 10 rounds exceeded €100M (with 10th Solaris at €140M), while in France only six of the Top 10 rounds were above €100M, with the 10th at €70M (Intact). This gap illustrates two approaches to scale: broad-based large rounds in Germany versus a more polarised concentration in France.

AI sits at the core of this shift. In 2025, AI investments reached €3 billion in France (+21%) and €3.03 billion in Germany (+38.3%), even as AI deal volumes declined in France (118 rounds, -24.4%) and increased modestly in Germany (283 rounds, +7.8%). This divergence confirms a decisive evolution: AI investment is no longer exploratory, but capital-intensive, infrastructure-driven and focused on real-economy deployment.

Focus on France: competitiveness through concentration and execution depth

France illustrates the most concentrated version of this transition. Out of €7.21 billion invested in French startups in 2025, €2.4 billion went to enterprise software tagged companies, and €1.7 billion to Mistral AI, nearly four times its 2024 funding (€468M). This level of concentration signals a clear shift: competitiveness is now built around a very limited number of execution-heavy platforms rather than broad application-layer innovation.

This dynamic is reinforced by the rapid rise of capital-intensive sectors. Semiconductors recorded one of the strongest accelerations (+420%), driven by next-generation hardware and computing rounds such as Alice & Bob (€100M) and Scintil Photonics (€50M), alongside a growing cluster of mid-sized industrial deeptech rounds. Robotics surged by +325%, supported by financings including Genesis AI (€95M) and Wandercraft (€68M), directly linking AI to industrial and healthcare execution.

Beyond enterprise software, health (€1.1B) and fintech (€715M) continued to attract substantial capital, particularly for payments infrastructure, compliance, diagnostics and biotech. The sustained presence of energy, transportation and food among the top funded sectors further confirms that, in France, AI is increasingly deployed as an optimisation and control layer within long-cycle physical systems, rather than as a standalone product.

Focus on Germany: competitiveness through diffusion and industrial scale

In Germany, €7.46 billion were invested in tech companies in 2025, following a more distributed model of capital deployment. Investment is spread across sectors, closely aligned with the country’s industrial backbone, supporting scale through interoperability and system-wide upgrading rather than platform concentration.

Robotics and education stand out as the strongest accelerators. Robotics funding jumped +432%, with deal count rising from 7 to 23, led by large rounds such as Quantum Systems (€340M), NEURA Robotics (€120M) and STARK (€56M), reinforcing Germany’s competitive edge in automation, defence and industrial equipment. Education technologies also rebounded strongly, reflecting renewed investor focus on workforce transformation, vocational training and enterprise learning - now viewed as essential competitiveness infrastructure in a technology-intensive economy.

Germany’s model is characterised by industrial diffusion: tech capital is embedded across manufacturing, logistics, energy systems and organisational processes, enabling long-term productivity gains across the real economy.

AI moves down the stack: one transition, two execution models

Across both countries, AI now represents a significant share of capital deployed in enterprise software, fintech, health, security and transportation, confirming its role as a core driver of performance rather than a technological option. In more infrastructure-heavy sectors such as energy, food and parts of transportation, AI adoption appears less visible in funding data, not due to weaker uptake, but because AI operates primarily as an operational layer, enhancing efficiency, predictability and resilience over long execution cycles.

“Once more, comparing tech investments in France and Germany proves that European competitiveness in AI is not built on a single model. France illustrates a more concentrated approach, where capital is deployed to accelerate execution in a limited number of large, execution-heavy projects. Germany, by contrast, follows a broader diffusion model, embedding innovation across its industrial backbone. Different paths, but the same requirement: the ability to quickly deploy AI at scale within real economic systems, over time and with direct results to justify the massive corporate investments.” explains Julien-David Nitlech, Managing Partner, IRIS

“It is now time to act. We must now significantly boost the funding capacity of French and German startups - an essential condition for innovative projects to scale and enhance Europe’s competitiveness in the international innovation race. Late-stage financing is indeed crucial for supporting startups in their scale-up phase. However, Series A+ fundraising has declined by 22% in France and 24% in Germany. We need to reverse this trend. And that’s what happens during the next VivaTech’s edition with Germany being “Country of the Year”. Thanks to a common Franco-German innovation ecosystem presentation, we are creating the necessary conditions for supporting the emergence of future European champions” declares Patrick Brandmaier, Managing director of the French-German Chamber of Commerce and Industry

Berlin, Paris – 22nd of February 2026 – IRIS, a leading European Venture and Growth investment firm, publishes the 2025 edition of “Financing Tech in Germany and France”.

By comparing Europe’s two largest tech and industrial economies over four consecutive years, relying on Dealroom data, the study shows that beyond cyclical fluctuations in funding volumes, European competitiveness is now defined by what capital is deployed for, not just where it is invested.

In 2025, France and Germany are undergoing the same structural transition: from software-led innovation to the transformation of real economic systems, while following two distinct execution paths.

Behind similar macro dynamics -capital concentration, rising AI intensity and tougher scaling conditions, the two countries reveal different ways of turning technology into economic performance and European competitiveness.

Fewer rounds, bigger bets: building Europe’s next tech champions

In 2025, total tech investments reached €7.21 billion in France (+2%) and €7.46 billion in Germany (stable year-on-year), despite a sharp contraction in deal activity (591 rounds in France, -24%; 1,426 rounds in Germany, -3%). This apparent paradox reflects a new competitive funding regime: fewer deals, but larger and more execution-intensive rounds.

Capital concentration has reached historically high levels. The Top 10 rounds accounted for 37% of total capital deployed in France (€2.58B) and 31% in Germany (€2.34B). The structure of this concentration differs markedly across the two markets. In Germany, all Top 10 rounds exceeded €100M (with 10th Solaris at €140M), while in France only six of the Top 10 rounds were above €100M, with the 10th at €70M (Intact). This gap illustrates two approaches to scale: broad-based large rounds in Germany versus a more polarised concentration in France.

AI sits at the core of this shift. In 2025, AI investments reached €3 billion in France (+21%) and €3.03 billion in Germany (+38.3%), even as AI deal volumes declined in France (118 rounds, -24.4%) and increased modestly in Germany (283 rounds, +7.8%). This divergence confirms a decisive evolution: AI investment is no longer exploratory, but capital-intensive, infrastructure-driven and focused on real-economy deployment.

Focus on France: competitiveness through concentration and execution depth

France illustrates the most concentrated version of this transition. Out of €7.21 billion invested in French startups in 2025, €2.4 billion went to enterprise software tagged companies, and €1.7 billion to Mistral AI, nearly four times its 2024 funding (€468M). This level of concentration signals a clear shift: competitiveness is now built around a very limited number of execution-heavy platforms rather than broad application-layer innovation.

This dynamic is reinforced by the rapid rise of capital-intensive sectors. Semiconductors recorded one of the strongest accelerations (+420%), driven by next-generation hardware and computing rounds such as Alice & Bob (€100M) and Scintil Photonics (€50M), alongside a growing cluster of mid-sized industrial deeptech rounds. Robotics surged by +325%, supported by financings including Genesis AI (€95M) and Wandercraft (€68M), directly linking AI to industrial and healthcare execution.

Beyond enterprise software, health (€1.1B) and fintech (€715M) continued to attract substantial capital, particularly for payments infrastructure, compliance, diagnostics and biotech. The sustained presence of energy, transportation and food among the top funded sectors further confirms that, in France, AI is increasingly deployed as an optimisation and control layer within long-cycle physical systems, rather than as a standalone product.

Focus on Germany: competitiveness through diffusion and industrial scale

In Germany, €7.46 billion were invested in tech companies in 2025, following a more distributed model of capital deployment. Investment is spread across sectors, closely aligned with the country’s industrial backbone, supporting scale through interoperability and system-wide upgrading rather than platform concentration.

Robotics and education stand out as the strongest accelerators. Robotics funding jumped +432%, with deal count rising from 7 to 23, led by large rounds such as Quantum Systems (€340M), NEURA Robotics (€120M) and STARK (€56M), reinforcing Germany’s competitive edge in automation, defence and industrial equipment. Education technologies also rebounded strongly, reflecting renewed investor focus on workforce transformation, vocational training and enterprise learning - now viewed as essential competitiveness infrastructure in a technology-intensive economy.

Germany’s model is characterised by industrial diffusion: tech capital is embedded across manufacturing, logistics, energy systems and organisational processes, enabling long-term productivity gains across the real economy.

AI moves down the stack: one transition, two execution models

Across both countries, AI now represents a significant share of capital deployed in enterprise software, fintech, health, security and transportation, confirming its role as a core driver of performance rather than a technological option. In more infrastructure-heavy sectors such as energy, food and parts of transportation, AI adoption appears less visible in funding data, not due to weaker uptake, but because AI operates primarily as an operational layer, enhancing efficiency, predictability and resilience over long execution cycles.

“Once more, comparing tech investments in France and Germany proves that European competitiveness in AI is not built on a single model. France illustrates a more concentrated approach, where capital is deployed to accelerate execution in a limited number of large, execution-heavy projects. Germany, by contrast, follows a broader diffusion model, embedding innovation across its industrial backbone. Different paths, but the same requirement: the ability to quickly deploy AI at scale within real economic systems, over time and with direct results to justify the massive corporate investments.” explains Julien-David Nitlech, Managing Partner, IRIS

“It is now time to act. We must now significantly boost the funding capacity of French and German startups - an essential condition for innovative projects to scale and enhance Europe’s competitiveness in the international innovation race. Late-stage financing is indeed crucial for supporting startups in their scale-up phase. However, Series A+ fundraising has declined by 22% in France and 24% in Germany. We need to reverse this trend. And that’s what happens during the next VivaTech’s edition with Germany being “Country of the Year”. Thanks to a common Franco-German innovation ecosystem presentation, we are creating the necessary conditions for supporting the emergence of future European champions” declares Patrick Brandmaier, Managing director of the French-German Chamber of Commerce and Industry

Financing Tech in Germany and France in 2025

The AI funding race is entering its industrial phase

Berlin, Paris – 22nd of February 2026 – IRIS, a leading European Venture and Growth investment firm, publishes the 2025 edition of “Financing Tech in Germany and France”.

By comparing Europe’s two largest tech and industrial economies over four consecutive years, relying on Dealroom data, the study shows that beyond cyclical fluctuations in funding volumes, European competitiveness is now defined by what capital is deployed for, not just where it is invested.

In 2025, France and Germany are undergoing the same structural transition: from software-led innovation to the transformation of real economic systems, while following two distinct execution paths.

Behind similar macro dynamics -capital concentration, rising AI intensity and tougher scaling conditions, the two countries reveal different ways of turning technology into economic performance and European competitiveness.

Fewer rounds, bigger bets: building Europe’s next tech champions

In 2025, total tech investments reached €7.21 billion in France (+2%) and €7.46 billion in Germany (stable year-on-year), despite a sharp contraction in deal activity (591 rounds in France, -24%; 1,426 rounds in Germany, -3%). This apparent paradox reflects a new competitive funding regime: fewer deals, but larger and more execution-intensive rounds.

Capital concentration has reached historically high levels. The Top 10 rounds accounted for 37% of total capital deployed in France (€2.58B) and 31% in Germany (€2.34B). The structure of this concentration differs markedly across the two markets. In Germany, all Top 10 rounds exceeded €100M (with 10th Solaris at €140M), while in France only six of the Top 10 rounds were above €100M, with the 10th at €70M (Intact). This gap illustrates two approaches to scale: broad-based large rounds in Germany versus a more polarised concentration in France.

AI sits at the core of this shift. In 2025, AI investments reached €3 billion in France (+21%) and €3.03 billion in Germany (+38.3%), even as AI deal volumes declined in France (118 rounds, -24.4%) and increased modestly in Germany (283 rounds, +7.8%). This divergence confirms a decisive evolution: AI investment is no longer exploratory, but capital-intensive, infrastructure-driven and focused on real-economy deployment.

Focus on France: competitiveness through concentration and execution depth

France illustrates the most concentrated version of this transition. Out of €7.21 billion invested in French startups in 2025, €2.4 billion went to enterprise software tagged companies, and €1.7 billion to Mistral AI, nearly four times its 2024 funding (€468M). This level of concentration signals a clear shift: competitiveness is now built around a very limited number of execution-heavy platforms rather than broad application-layer innovation.

This dynamic is reinforced by the rapid rise of capital-intensive sectors. Semiconductors recorded one of the strongest accelerations (+420%), driven by next-generation hardware and computing rounds such as Alice & Bob (€100M) and Scintil Photonics (€50M), alongside a growing cluster of mid-sized industrial deeptech rounds. Robotics surged by +325%, supported by financings including Genesis AI (€95M) and Wandercraft (€68M), directly linking AI to industrial and healthcare execution.

Beyond enterprise software, health (€1.1B) and fintech (€715M) continued to attract substantial capital, particularly for payments infrastructure, compliance, diagnostics and biotech. The sustained presence of energy, transportation and food among the top funded sectors further confirms that, in France, AI is increasingly deployed as an optimisation and control layer within long-cycle physical systems, rather than as a standalone product.

Focus on Germany: competitiveness through diffusion and industrial scale

In Germany, €7.46 billion were invested in tech companies in 2025, following a more distributed model of capital deployment. Investment is spread across sectors, closely aligned with the country’s industrial backbone, supporting scale through interoperability and system-wide upgrading rather than platform concentration.

Robotics and education stand out as the strongest accelerators. Robotics funding jumped +432%, with deal count rising from 7 to 23, led by large rounds such as Quantum Systems (€340M), NEURA Robotics (€120M) and STARK (€56M), reinforcing Germany’s competitive edge in automation, defence and industrial equipment. Education technologies also rebounded strongly, reflecting renewed investor focus on workforce transformation, vocational training and enterprise learning - now viewed as essential competitiveness infrastructure in a technology-intensive economy.

Germany’s model is characterised by industrial diffusion: tech capital is embedded across manufacturing, logistics, energy systems and organisational processes, enabling long-term productivity gains across the real economy.

AI moves down the stack: one transition, two execution models

Across both countries, AI now represents a significant share of capital deployed in enterprise software, fintech, health, security and transportation, confirming its role as a core driver of performance rather than a technological option. In more infrastructure-heavy sectors such as energy, food and parts of transportation, AI adoption appears less visible in funding data, not due to weaker uptake, but because AI operates primarily as an operational layer, enhancing efficiency, predictability and resilience over long execution cycles.

“Once more, comparing tech investments in France and Germany proves that European competitiveness in AI is not built on a single model. France illustrates a more concentrated approach, where capital is deployed to accelerate execution in a limited number of large, execution-heavy projects. Germany, by contrast, follows a broader diffusion model, embedding innovation across its industrial backbone. Different paths, but the same requirement: the ability to quickly deploy AI at scale within real economic systems, over time and with direct results to justify the massive corporate investments.” explains Julien-David Nitlech, Managing Partner, IRIS

“It is now time to act. We must now significantly boost the funding capacity of French and German startups - an essential condition for innovative projects to scale and enhance Europe’s competitiveness in the international innovation race. Late-stage financing is indeed crucial for supporting startups in their scale-up phase. However, Series A+ fundraising has declined by 22% in France and 24% in Germany. We need to reverse this trend. And that’s what happens during the next VivaTech’s edition with Germany being “Country of the Year”. Thanks to a common Franco-German innovation ecosystem presentation, we are creating the necessary conditions for supporting the emergence of future European champions” declares Patrick Brandmaier, Managing director of the French-German Chamber of Commerce and Industry

Berlin, Paris – 22nd of February 2026 – IRIS, a leading European Venture and Growth investment firm, publishes the 2025 edition of “Financing Tech in Germany and France”.

By comparing Europe’s two largest tech and industrial economies over four consecutive years, relying on Dealroom data, the study shows that beyond cyclical fluctuations in funding volumes, European competitiveness is now defined by what capital is deployed for, not just where it is invested.

In 2025, France and Germany are undergoing the same structural transition: from software-led innovation to the transformation of real economic systems, while following two distinct execution paths.

Behind similar macro dynamics -capital concentration, rising AI intensity and tougher scaling conditions, the two countries reveal different ways of turning technology into economic performance and European competitiveness.

Fewer rounds, bigger bets: building Europe’s next tech champions

In 2025, total tech investments reached €7.21 billion in France (+2%) and €7.46 billion in Germany (stable year-on-year), despite a sharp contraction in deal activity (591 rounds in France, -24%; 1,426 rounds in Germany, -3%). This apparent paradox reflects a new competitive funding regime: fewer deals, but larger and more execution-intensive rounds.

Capital concentration has reached historically high levels. The Top 10 rounds accounted for 37% of total capital deployed in France (€2.58B) and 31% in Germany (€2.34B). The structure of this concentration differs markedly across the two markets. In Germany, all Top 10 rounds exceeded €100M (with 10th Solaris at €140M), while in France only six of the Top 10 rounds were above €100M, with the 10th at €70M (Intact). This gap illustrates two approaches to scale: broad-based large rounds in Germany versus a more polarised concentration in France.

AI sits at the core of this shift. In 2025, AI investments reached €3 billion in France (+21%) and €3.03 billion in Germany (+38.3%), even as AI deal volumes declined in France (118 rounds, -24.4%) and increased modestly in Germany (283 rounds, +7.8%). This divergence confirms a decisive evolution: AI investment is no longer exploratory, but capital-intensive, infrastructure-driven and focused on real-economy deployment.

Focus on France: competitiveness through concentration and execution depth

France illustrates the most concentrated version of this transition. Out of €7.21 billion invested in French startups in 2025, €2.4 billion went to enterprise software tagged companies, and €1.7 billion to Mistral AI, nearly four times its 2024 funding (€468M). This level of concentration signals a clear shift: competitiveness is now built around a very limited number of execution-heavy platforms rather than broad application-layer innovation.

This dynamic is reinforced by the rapid rise of capital-intensive sectors. Semiconductors recorded one of the strongest accelerations (+420%), driven by next-generation hardware and computing rounds such as Alice & Bob (€100M) and Scintil Photonics (€50M), alongside a growing cluster of mid-sized industrial deeptech rounds. Robotics surged by +325%, supported by financings including Genesis AI (€95M) and Wandercraft (€68M), directly linking AI to industrial and healthcare execution.

Beyond enterprise software, health (€1.1B) and fintech (€715M) continued to attract substantial capital, particularly for payments infrastructure, compliance, diagnostics and biotech. The sustained presence of energy, transportation and food among the top funded sectors further confirms that, in France, AI is increasingly deployed as an optimisation and control layer within long-cycle physical systems, rather than as a standalone product.

Focus on Germany: competitiveness through diffusion and industrial scale

In Germany, €7.46 billion were invested in tech companies in 2025, following a more distributed model of capital deployment. Investment is spread across sectors, closely aligned with the country’s industrial backbone, supporting scale through interoperability and system-wide upgrading rather than platform concentration.

Robotics and education stand out as the strongest accelerators. Robotics funding jumped +432%, with deal count rising from 7 to 23, led by large rounds such as Quantum Systems (€340M), NEURA Robotics (€120M) and STARK (€56M), reinforcing Germany’s competitive edge in automation, defence and industrial equipment. Education technologies also rebounded strongly, reflecting renewed investor focus on workforce transformation, vocational training and enterprise learning - now viewed as essential competitiveness infrastructure in a technology-intensive economy.

Germany’s model is characterised by industrial diffusion: tech capital is embedded across manufacturing, logistics, energy systems and organisational processes, enabling long-term productivity gains across the real economy.

AI moves down the stack: one transition, two execution models

Across both countries, AI now represents a significant share of capital deployed in enterprise software, fintech, health, security and transportation, confirming its role as a core driver of performance rather than a technological option. In more infrastructure-heavy sectors such as energy, food and parts of transportation, AI adoption appears less visible in funding data, not due to weaker uptake, but because AI operates primarily as an operational layer, enhancing efficiency, predictability and resilience over long execution cycles.

“Once more, comparing tech investments in France and Germany proves that European competitiveness in AI is not built on a single model. France illustrates a more concentrated approach, where capital is deployed to accelerate execution in a limited number of large, execution-heavy projects. Germany, by contrast, follows a broader diffusion model, embedding innovation across its industrial backbone. Different paths, but the same requirement: the ability to quickly deploy AI at scale within real economic systems, over time and with direct results to justify the massive corporate investments.” explains Julien-David Nitlech, Managing Partner, IRIS

“It is now time to act. We must now significantly boost the funding capacity of French and German startups - an essential condition for innovative projects to scale and enhance Europe’s competitiveness in the international innovation race. Late-stage financing is indeed crucial for supporting startups in their scale-up phase. However, Series A+ fundraising has declined by 22% in France and 24% in Germany. We need to reverse this trend. And that’s what happens during the next VivaTech’s edition with Germany being “Country of the Year”. Thanks to a common Franco-German innovation ecosystem presentation, we are creating the necessary conditions for supporting the emergence of future European champions” declares Patrick Brandmaier, Managing director of the French-German Chamber of Commerce and Industry

Berlin, Paris – 22nd of February 2026 – IRIS, a leading European Venture and Growth investment firm, publishes the 2025 edition of “Financing Tech in Germany and France”.

By comparing Europe’s two largest tech and industrial economies over four consecutive years, relying on Dealroom data, the study shows that beyond cyclical fluctuations in funding volumes, European competitiveness is now defined by what capital is deployed for, not just where it is invested.

In 2025, France and Germany are undergoing the same structural transition: from software-led innovation to the transformation of real economic systems, while following two distinct execution paths.

Behind similar macro dynamics -capital concentration, rising AI intensity and tougher scaling conditions, the two countries reveal different ways of turning technology into economic performance and European competitiveness.

Fewer rounds, bigger bets: building Europe’s next tech champions

In 2025, total tech investments reached €7.21 billion in France (+2%) and €7.46 billion in Germany (stable year-on-year), despite a sharp contraction in deal activity (591 rounds in France, -24%; 1,426 rounds in Germany, -3%). This apparent paradox reflects a new competitive funding regime: fewer deals, but larger and more execution-intensive rounds.

Capital concentration has reached historically high levels. The Top 10 rounds accounted for 37% of total capital deployed in France (€2.58B) and 31% in Germany (€2.34B). The structure of this concentration differs markedly across the two markets. In Germany, all Top 10 rounds exceeded €100M (with 10th Solaris at €140M), while in France only six of the Top 10 rounds were above €100M, with the 10th at €70M (Intact). This gap illustrates two approaches to scale: broad-based large rounds in Germany versus a more polarised concentration in France.

AI sits at the core of this shift. In 2025, AI investments reached €3 billion in France (+21%) and €3.03 billion in Germany (+38.3%), even as AI deal volumes declined in France (118 rounds, -24.4%) and increased modestly in Germany (283 rounds, +7.8%). This divergence confirms a decisive evolution: AI investment is no longer exploratory, but capital-intensive, infrastructure-driven and focused on real-economy deployment.

Focus on France: competitiveness through concentration and execution depth

France illustrates the most concentrated version of this transition. Out of €7.21 billion invested in French startups in 2025, €2.4 billion went to enterprise software tagged companies, and €1.7 billion to Mistral AI, nearly four times its 2024 funding (€468M). This level of concentration signals a clear shift: competitiveness is now built around a very limited number of execution-heavy platforms rather than broad application-layer innovation.

This dynamic is reinforced by the rapid rise of capital-intensive sectors. Semiconductors recorded one of the strongest accelerations (+420%), driven by next-generation hardware and computing rounds such as Alice & Bob (€100M) and Scintil Photonics (€50M), alongside a growing cluster of mid-sized industrial deeptech rounds. Robotics surged by +325%, supported by financings including Genesis AI (€95M) and Wandercraft (€68M), directly linking AI to industrial and healthcare execution.

Beyond enterprise software, health (€1.1B) and fintech (€715M) continued to attract substantial capital, particularly for payments infrastructure, compliance, diagnostics and biotech. The sustained presence of energy, transportation and food among the top funded sectors further confirms that, in France, AI is increasingly deployed as an optimisation and control layer within long-cycle physical systems, rather than as a standalone product.

Focus on Germany: competitiveness through diffusion and industrial scale

In Germany, €7.46 billion were invested in tech companies in 2025, following a more distributed model of capital deployment. Investment is spread across sectors, closely aligned with the country’s industrial backbone, supporting scale through interoperability and system-wide upgrading rather than platform concentration.

Robotics and education stand out as the strongest accelerators. Robotics funding jumped +432%, with deal count rising from 7 to 23, led by large rounds such as Quantum Systems (€340M), NEURA Robotics (€120M) and STARK (€56M), reinforcing Germany’s competitive edge in automation, defence and industrial equipment. Education technologies also rebounded strongly, reflecting renewed investor focus on workforce transformation, vocational training and enterprise learning - now viewed as essential competitiveness infrastructure in a technology-intensive economy.

Germany’s model is characterised by industrial diffusion: tech capital is embedded across manufacturing, logistics, energy systems and organisational processes, enabling long-term productivity gains across the real economy.

AI moves down the stack: one transition, two execution models

Across both countries, AI now represents a significant share of capital deployed in enterprise software, fintech, health, security and transportation, confirming its role as a core driver of performance rather than a technological option. In more infrastructure-heavy sectors such as energy, food and parts of transportation, AI adoption appears less visible in funding data, not due to weaker uptake, but because AI operates primarily as an operational layer, enhancing efficiency, predictability and resilience over long execution cycles.

“Once more, comparing tech investments in France and Germany proves that European competitiveness in AI is not built on a single model. France illustrates a more concentrated approach, where capital is deployed to accelerate execution in a limited number of large, execution-heavy projects. Germany, by contrast, follows a broader diffusion model, embedding innovation across its industrial backbone. Different paths, but the same requirement: the ability to quickly deploy AI at scale within real economic systems, over time and with direct results to justify the massive corporate investments.” explains Julien-David Nitlech, Managing Partner, IRIS

“It is now time to act. We must now significantly boost the funding capacity of French and German startups - an essential condition for innovative projects to scale and enhance Europe’s competitiveness in the international innovation race. Late-stage financing is indeed crucial for supporting startups in their scale-up phase. However, Series A+ fundraising has declined by 22% in France and 24% in Germany. We need to reverse this trend. And that’s what happens during the next VivaTech’s edition with Germany being “Country of the Year”. Thanks to a common Franco-German innovation ecosystem presentation, we are creating the necessary conditions for supporting the emergence of future European champions” declares Patrick Brandmaier, Managing director of the French-German Chamber of Commerce and Industry